By Phil Ganz

By Phil Ganz

Edited by Ryan Skerritt

Edited by Ryan Skerritt

This guide aims to clarify the role of residual income in the VA loan process, from calculation to its impact on loan eligibility and the importance of family size.

By understanding these elements, applicants can better navigate the requirements, enhancing their journey toward sustainable homeownership.

Table of Contents

What is Residual Income?

Residual income refers to the net income remaining each month after paying all monthly debts and living expenses.

There are a number of types of debts that fall under this category, including but not limited to credit cards, car loans, personal loans, and monthly mortgage payments.

Basically, it measures a borrower's financial health by showing how much money is left over after meeting essential expenses.

In the VA loan approval process, residual income plays a vital role in evaluating a borrower's financial status.

Unlike traditional lending metrics, which rely heavily on credit scores and debt-to-income ratios, the VA loan program uses residual income as a more holistic measure of borrowers' ability to manage their finances.

Using this approach helps ensure veterans and their families are not only qualified for a home loan but also maintain financial stability and comfort after purchasing a home.

By emphasizing residual income, the VA reduces default risk by ensuring borrowers have sufficient funds to handle unforeseen expenses.

Residual Income vs. Gross Income

It's important to distinguish between residual and gross income, as they are two very different indicators of financial health. Gross income is the total income earned before any deductions, taxes, or expenses are accounted for.

In contrast, residual income is calculated after all monthly debts and living expenses have been paid, providing a clearer picture of the borrower's disposable income.

While gross income gives an overview of a borrower's earnings, residual income offers a more accurate insight into their financial stability and ability to afford ongoing homeownership costs.

By focusing on residual income, the VA loan program ensures that veterans and active military members are better positioned to manage their mortgages and maintain a comfortable lifestyle, safeguarding them against financial hardship.

How Residual Income Affects VA Loan Eligibility

A borrower's residual income plays a critical role in determining eligibility for a VA loan, ensuring sufficient funds to cover living expenses after monthly debt payments are made.

The VA loan program emphasizes residual income significantly more than traditional lending practices that primarily focus on credit scores and debt-to-income (DTI) ratios.

By combining residual income with other financial assessments, the VA can assess a borrower's financial position more comprehensively.

Borrowers who meet the VA's residual income requirements are considered less likely to face financial difficulties after obtaining a loan, making them a lower risk for lenders.

This means borrowers with higher residual income levels may be able to overcome other financial weaknesses, such as high debt-to-income ratios or not-perfect credit scores.

The VA’s Residual Income Guidelines and Requirements

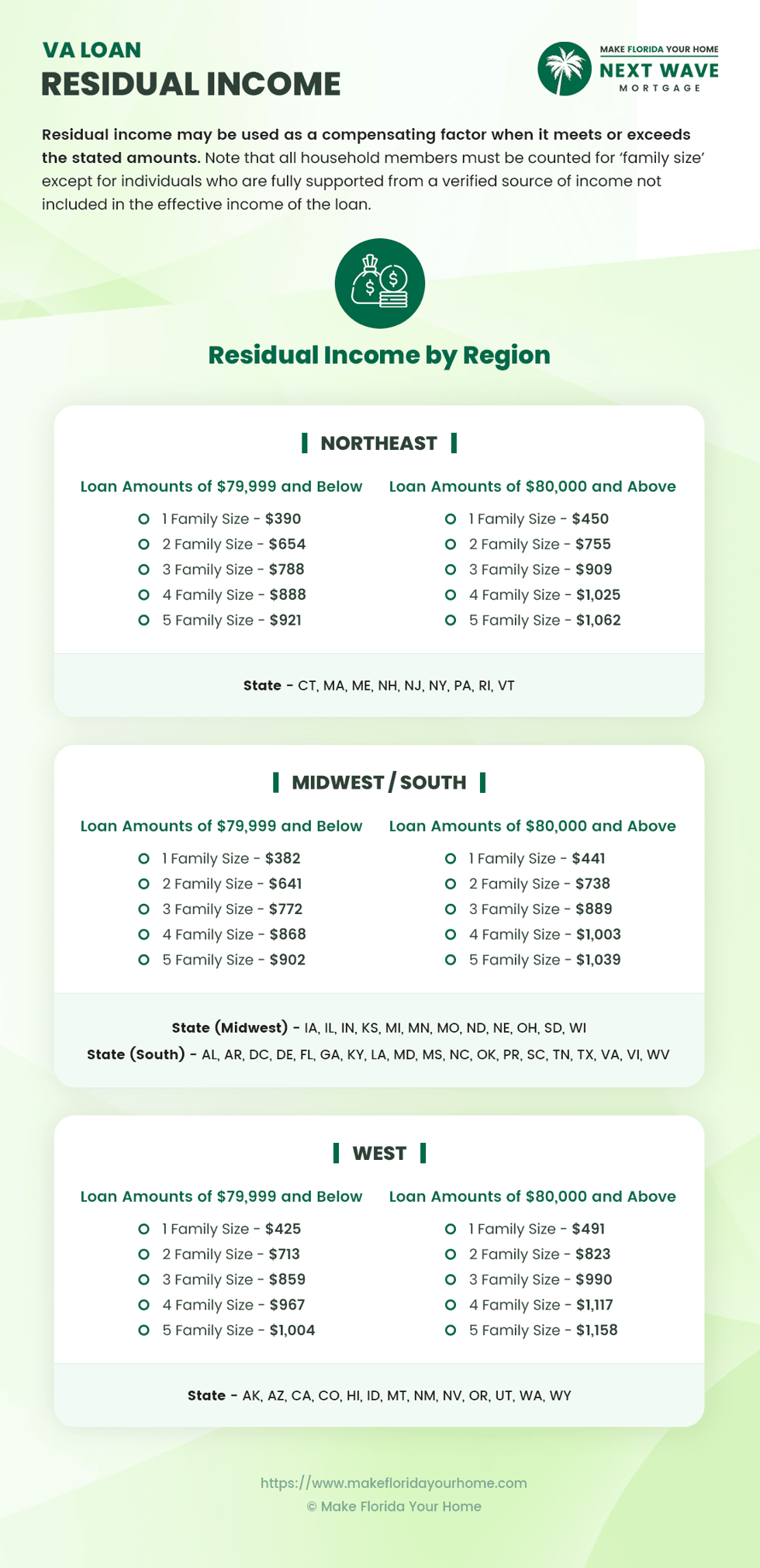

The Department of Veterans Affairs has established specific residual income guidelines that borrowers must meet or exceed to qualify for a VA loan.

These guidelines vary based on family size, loan amount, and region of the country, reflecting the cost of living differences across the United States.

The VA’s residual income requirements ensure borrowers have enough money each month to cover basic living expenses, including food, transportation, and childcare.

Lenders subtract all monthly debt payments and housing expenses from the borrower's gross monthly income to calculate residual income. The remaining amount is then compared to the VA's minimum residual income thresholds.

Borrowers must meet or exceed these minimums to qualify for a VA loan. It's important to note that the required residual income amount increases with larger family sizes and regions with a higher cost of living.

Step-by-Step Guide to Calculating Residual Income

Calculating residual income is a crucial step for prospective VA loan applicants. This process ensures that borrowers have monthly disposable income to cover their living expenses after paying their debts.

Here's how to calculate residual income for VA loans:

-

Determine Gross Monthly Income: Start by calculating your total gross monthly income, including all income sources before taxes and other deductions. This includes military pay, civilian pay, retirement income, investment income, and other regular sources.

-

List Monthly Debts and Obligations: Compile a list of your monthly debts, such as mortgage or rent payments, car loans, credit card payments, student loans, and any other recurring debt obligations.

-

Subtract Monthly Debts from Gross Monthly Income: Deduct the total monthly debts from your gross monthly income to get your net income.

-

Account for Estimated Monthly Living Expenses: Subtract estimated monthly living expenses, including utilities, groceries, insurance, and childcare, from the net income. The remaining amount is your residual income.

- Compare to VA Residual Income Guidelines: Finally, compare your calculated residual income to the VA's minimum residual income requirements for your loan amount, family size, and geographical region.

Examples of Common Expenses and Debts to Consider

When calculating your residual income, including a comprehensive list of debts and living expenses is important.

Here are some common examples:

-

Housing Expenses: Mortgage or rent, property taxes, homeowners insurance, and homeowners association (HOA) fees.

-

Loan Payments: Car loans, student loans, personal loans, and other installment debts.

-

Credit Card Payments: Minimum monthly payments on credit card debts.

-

Utilities and Household Expenses: Electricity, water, gas, internet, cable, and phone bills.

- Daily Living Costs: Groceries, transportation, childcare, healthcare, and other essential expenses.

Family Size and Its Impact on Residual Income

In the context of VA loans, "family size" refers to the number of individuals in a borrower's household who depend on the borrower's income for living expenses. This number is crucial in determining the residual income requirements of the Department of Veterans Affairs.

The VA's guidelines ensure that veterans have sufficient income to support their dependents while maintaining a certain standard of living.

As family size increases, so does the minimum residual income requirement, reflecting the higher living costs associated with supporting more individuals.

The VA loan program allows for certain exclusions when calculating family size, recognizing that not all household members may depend on the borrower's income. These exclusions can lower the borrower's residual income requirement by reducing the official family size.

Two common scenarios illustrate how exclusions can apply:

Scenario: Spouse Not Obligated on the Note

If a spouse is not obligated on the VA loan note and has a stable and reliable income that can support their living expenses independently, they may be excluded from the family size calculation.

This situation acknowledges the spouse's financial contribution to the household, allowing for a more accurate assessment of the borrower's residual income requirements.

Scenario: Children with Alternative Support

Children in the household who receive sufficient support through other verified income sources, such as foster care payments or regular child support, may also be excluded from the family size calculation.

This reflects the reality that the borrower's income is not the sole source of support for these dependents, potentially reducing the residual income requirement for the loan.

Frequently Asked Questions about Residual Income and VA Loans

Understanding these aspects of residual income and family size calculations is essential for navigating the VA loan process.

By equipping yourself with this knowledge, you can better prepare for a successful VA loan application and sustainable homeownership.

What is Residual Income in the Context of VA Loans?

Residual income for VA loans refers to the money left over each month after a borrower has paid all personal debts and living expenses.

It's a measure the VA uses to ensure veterans have enough income to handle life's necessities beyond their mortgage payments.

Why is Residual Income Important for VA Loan Approval?

Residual income is crucial because it helps gauge a borrower's financial stability and ability to sustain homeownership.

The VA uses it to prevent veterans from becoming overburdened by their mortgage by ensuring they have sufficient disposable income each month.

How Do I Calculate My Residual Income for a VA Loan?

To calculate your residual income, subtract your monthly debts and living expenses from your gross monthly income.

The remaining amount is your residual income. Consider using VA loan calculators or consult with a loan specialist for precise calculations.

What Are the VA's Residual Income Guidelines?

The VA's residual income guidelines vary by region, family size, and loan amount. These guidelines ensure that borrowers have enough income left each month to cover basic living expenses.

Check the latest VA charts or consult with a loan officer for specific figures.

Can Family Size Affect My VA Loan Residual Income Requirements?

Yes, family size significantly impacts residual income requirements.

Larger families have higher residual income thresholds to meet, reflecting the increased costs associated with supporting more dependents.

Are There Any Exclusions When Calculating Family Size for a VA Loan?

Yes, certain individuals can be excluded from the family size calculation, such as a spouse with independent income not obligated on the loan or children who receive sufficient support from other sources like child support or foster care payments.

What Happens If I Don't Meet the VA's Residual Income Requirements?

Falling short of the VA's residual income requirements might affect your loan approval.

However, lenders may consider other factors, like exceptional credit or significant savings, as compensating factors.

Can a Spouse's Income Be Included in Residual Income Calculations?

Yes, a spouse's income can be included if they are obligated on the loan or if it significantly contributes to the household's residual income, providing they share the same residence.

How Do Regional Variations Affect Residual Income Requirements?

The VA adjusts residual income requirements based on the cost of living in different regions of the country. Borrowers in areas with a higher cost of living will face higher residual income thresholds.

Where Can I Find Tools and Resources to Help Calculate My Residual Income?

Various online resources, including VA loan residual income calculators, can help you estimate your residual income.

Additionally, consulting with a VA loan specialist or financial advisor can provide personalized assistance and clarity.

Conclusion

Understanding residual income and how it impacts VA loan eligibility is essential for veterans and military families looking to buy a home.

Applicants are better positioned to meet the VA's requirements when they understand the significance of residual income, calculate it accurately, and recognize how family size affects these calculations.

Remember, the goal is not just to secure a loan but to ensure sustainable homeownership and financial stability for those who have served our country.

Armed with this knowledge, you're ready to take the next steps toward securing a home with the benefits you've earned through your service.

With over 50 years of mortgage industry experience, we are here to help you achieve the American dream of owning a home. We strive to provide the best education before, during, and after you buy a home. Our advice is based on experience with Phil Ganz and Team closing over One billion dollars and helping countless families.

About Author - Phil Ganz

Phil Ganz has over 20+ years of experience in the residential financing space. With over a billion dollars of funded loans, Phil helps homebuyers configure the perfect mortgage plan. Whether it's your first home, a complex multiple-property purchase, or anything in between, Phil has the experience to help you achieve your goals.

About Editor - Ryan Skerritt

Ryan Skerritt has over 10+ years of experience in the residential financing space. With over two hundred and fifty million of funded loan volume, Ryan has the skill set to help any homebuyer configure the perfect mortgage plan.