By Phil Ganz

By Phil Ganz

Edited by Ryan Skerritt

Edited by Ryan Skerritt

Whether it's the basic occupancy rules or more complex situations like deployments or extended absences, we'll cover everything you need to know.

What Are the VA Loan Residence Occupancy Requirements?

Utilizing a VA loan to acquire a home mandates that the property must function as the buyer's primary residence, excluding the possibility of using it for secondary or investment purposes.

The expectation is for the buyer to take residence in the newly purchased home promptly, typically setting this period at no more than 60 days following the property's closing.

In scenarios where imminent repairs or renovations delay the buyer's ability to occupy the home, this deviation from the standard occupancy timeline is labeled a "delay."

Consequently, such delays might lead to the mortgage lender requesting additional documentation to address the postponement in fulfilling the occupancy criteria.

Requirements For Families

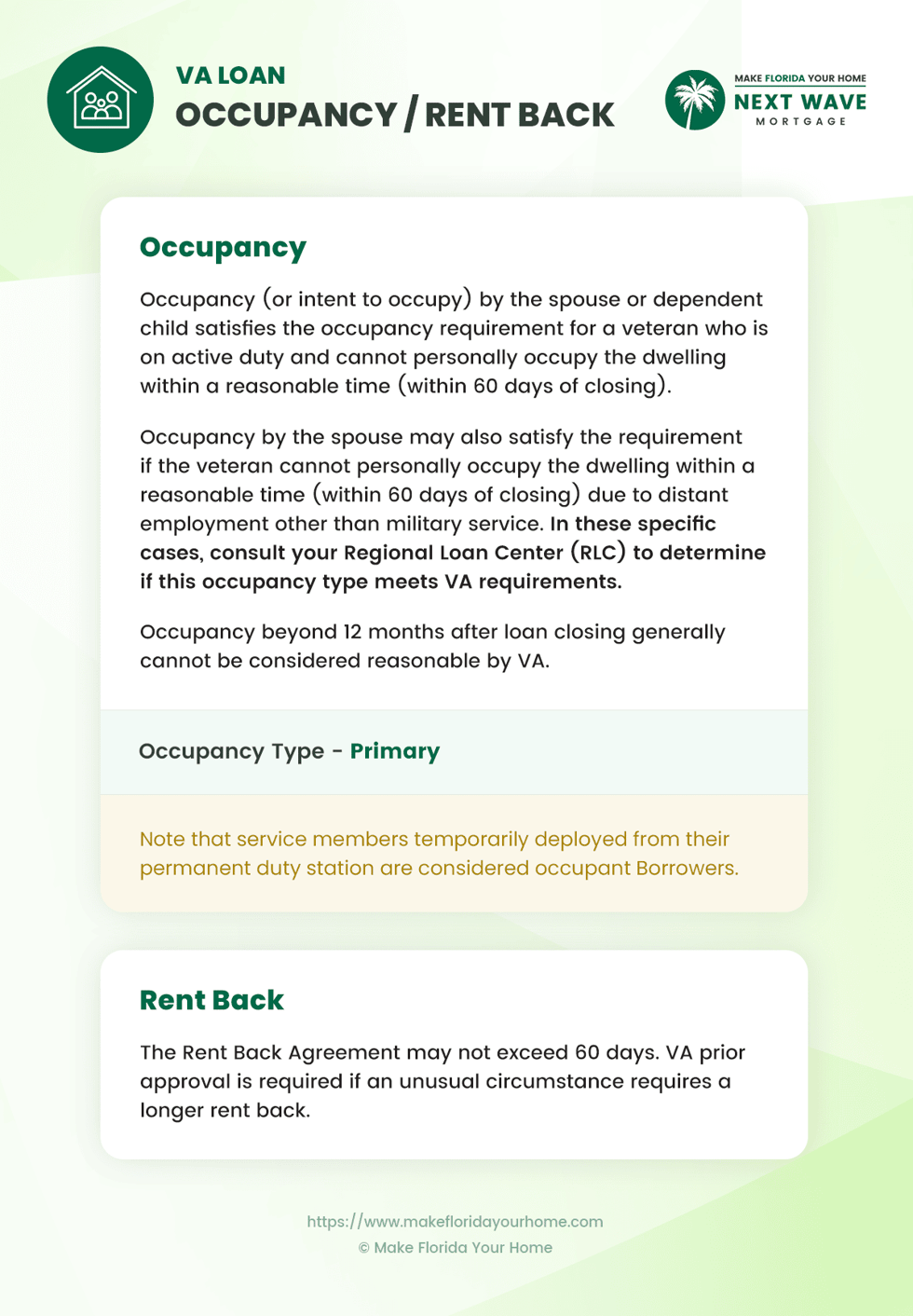

For families of veterans or active service members, the VA loan occupancy requirements offer flexibility. A spouse or dependent child can satisfy the occupancy requirement if the veteran cannot occupy the home due to service obligations or other valid reasons.

This provision ensures that families can still benefit from VA loans even when the service member is deployed or stationed away from home.

The veteran needs to provide certification of the intent to occupy the home as soon as possible, ensuring compliance with VA guidelines.

Requirements For Refinanced VA Loans

Occupancy regulations under the VA loan program have specific implications for various refinancing options, though they vary by type.

For a VA cash-out refinance, borrowers must undergo a fresh appraisal and credit evaluation, demonstrating that the refinanced property will serve as their primary residence.

The VA Interest Rate Reduction Refinance Loan (IRL), commonly called the VA Streamline Refinance, simplifies the process. Here, the borrower is only required to verify that the property served as their primary residence during the tenure of the initial VA loan.

This refinance offers several benefits, including securing lower interest rates, reducing monthly payments, and other financial improvements.

Requirements For Deployed Active-Duty Service Members

Deployed active-duty service members face unique challenges in meeting the VA loan occupancy requirements.

Recognizing this, the VA considers a service member deployed from their permanent duty station as occupying the home, provided they intend to return. This provision ensures that those serving our country can still access VA loan benefits without penalty for their service.

Documentation and communication with the lender are key to satisfying these requirements, ensuring service members can focus on their duties without worrying about home loan compliance.

Special Occupancy Situations

The VA acknowledges that special circumstances may affect veterans' ability to meet the standard occupancy requirements.

One such situation is the "Rent Back Agreement," which cannot exceed 60 days. This agreement allows the veteran to temporarily rent the property to the seller, providing additional flexibility in moving situations.

However, any rent-back period longer than 60 days requires prior approval from the VA, typically only granted in unusual circumstances. Veterans facing unique occupancy challenges should consult with their lender and the VA to explore possible accommodations.

How Does the VA Determine Occupancy?

When purchasing a property with a VA loan, the fundamental requirement is that the home must be your primary residence.

This means that properties intended as second homes or for investment purposes are not eligible for financing through a VA home loan.

A key aspect of meeting the VA's occupancy requirements is the timeline for moving into the purchased property.

The VA mandates that new homeowners occupy their homes within what is considered a reasonable timeframe, which is generally expected to be within 60 days following the house's closing.

How Does a VA Loan Verify Occupancy?

Verifying occupancy is a critical step in securing a VA loan, as the program is designed to ensure that the financed property is used as the borrower's primary residence.

Typically, this involves requesting a letter from the borrower explicitly stating their intention to make the property their primary residence.

After a period of one year of residence, borrowers are given the flexibility to convert their property into an investment property by renting it out.

This provision allows veterans to leverage their property as a financial asset, opening up opportunities for generating income while still adhering to the rules and regulations of the VA loan program in the initial occupancy period.

Can There Be a Non-Occupant Co-Borrower on a VA Loan?

Civilians are generally not permitted to co-sign a VA loan, with the sole exception being the spouse of the veteran or service member.

This exception allows spouses to jointly apply for a VA loan, enhancing the borrowing power and potentially qualifying for a larger loan amount or better terms.

Additionally, if another veteran is considered as a co-borrower, there is a critical requirement that they must also reside in the property.

This ensures that all individuals co-borrowing under the VA loan program actively use the home as their primary residence.

The emphasis on occupancy by co-borrowers aligns with the VA loan program's overarching goal to assist veterans and their immediate families in securing and maintaining homeownership.

What Qualifies as a Primary Residence?

Understanding the definition of a primary residence is essential, especially when considering loan applications or tax implications. A primary residence is recognized legally as the main or principal home you reside in for most of the year.

The criteria for a property to be considered your primary residence are straightforward but strict; you can only designate one property as such at any given time.

This designation is typically evidenced by the address on your driver's license, tax returns, and other significant government documents.

These documents serve as proof points to various institutions, indicating that the home you claim as your primary residence is your main living space.

This classification has significant implications for financial, legal, and tax-related matters, making it a critical consideration for homeowners.

Can a Veteran Have Two Primary Residences?

There are specific conditions under which a veteran can hold two VA loans simultaneously. The key condition is that both properties financed under VA loans must qualify as the borrower's primary residence.

This scenario generally applies to active service members who receive Permanent Change of Station (PCS) orders, allowing them to maintain two homes under certain circumstances.

This provision recognizes the unique needs of military personnel who may be required to relocate frequently while still owning a home in another location. It's designed to ensure veterans and active duty service members can secure housing for themselves and their families.

The ability to have two VA loans at once under these conditions underscores the program's commitment to providing flexible housing solutions to those who serve.

FAQ: VA Loan Occupancy Requirements in 2024

Our readers most asked questions about VA loan occupancy requirements:

Is it mandatory to have a physical inspection for VA loan occupancy verification?

No, physical inspections are not always mandatory for VA loan occupancy verification. Lenders typically require a written statement or certification from the borrower affirming their intent to occupy the home as their primary residence.

Can a veteran use a VA loan to buy a fixer-upper as a primary residence?

Veterans can use a VA loan to buy a fixer-upper, provided they intend to make it their primary residence. However, the property must meet the VA's minimum property requirements and may require a VA-approved contractor to complete necessary repairs.

Are there any exceptions to the 60-day occupancy rule for new constructions?

Yes, the VA may offer flexibility for new constructions, recognizing that building a home can take longer than 60 days. Veterans should communicate with their lender to obtain specific guidance and potential extensions.

How do PCS orders affect VA loan occupancy for service members?

PCS orders allow service members to qualify for a new VA loan for a residence in their new location, even if they have an existing VA loan, acknowledging the unique circumstances of military service.

What happens if a veteran cannot occupy the home within the required timeframe due to unforeseen circumstances?

Veterans facing unforeseen circumstances should immediately communicate with their lender. The VA offers flexibility in certain situations, and lenders may provide extensions or alternative solutions on a case-by-case basis.

Can a veteran's parent satisfy the occupancy requirement in the veteran's absence?

Only a veteran's spouse or dependent can typically satisfy the occupancy requirement. However, exceptions may be considered under special circumstances, requiring direct consultation with the lender and VA approval.

How does divorce affect VA loan occupancy requirements?

In the event of a divorce, if the veteran is not living in the home, they may need to refinance or make arrangements to ensure compliance with VA occupancy requirements. Legal advice and lender consultation are advisable.

Can veterans apply for a VA loan if they plan to retire and occupy the home within a year?

Yes, veterans planning to retire and occupy the home within a reasonable timeframe, typically within 12 months, can discuss their situation with their lender to meet occupancy requirements.

Are there occupancy considerations for VA loans used for home improvements?

For VA loans specifically for home improvements, the veteran must still certify the property as their primary residence, ensuring the loan is used to improve their primary home.

What documentation is required to prove occupancy for a VA loan?

Documentation can include a signed certification of intent to occupy, utility bills in the borrower's name, or other government documents proving the property is the primary residence.

Bottom Line

Getting a VA loan in 2024 means knowing a few key rules about where you can live. Your new home must be the main place you live, not a second home or a place you plan to rent out.

You should move in within 60 days after you buy it, but there are special cases, like if you're deployed or doing major repairs.

This guide has covered the essentials, from buying your first home and handling moves due to military service to refinancing your house. These rules are there to make sure VA loans help those who've served to get into homes they'll really live in.

Talking to MakeFloridaYourHome or the VA can help clear things up if you're stuck or your situation is different. We're here to help you stay on track and correctly use your VA loan benefits.

With over 50 years of mortgage industry experience, we are here to help you achieve the American dream of owning a home. We strive to provide the best education before, during, and after you buy a home. Our advice is based on experience with Phil Ganz and Team closing over One billion dollars and helping countless families.

About Author - Phil Ganz

Phil Ganz has over 20+ years of experience in the residential financing space. With over a billion dollars of funded loans, Phil helps homebuyers configure the perfect mortgage plan. Whether it's your first home, a complex multiple-property purchase, or anything in between, Phil has the experience to help you achieve your goals.

About Editor - Ryan Skerritt

Ryan Skerritt has over 10+ years of experience in the residential financing space. With over two hundred and fifty million of funded loan volume, Ryan has the skill set to help any homebuyer configure the perfect mortgage plan.