By Phil Ganz

By Phil Ganz

Edited by Ryan Skerritt

Edited by Ryan Skerritt

Gift funds, which can be used for down payments and closing costs, can be a great way to lessen the burden of buying a home as a veteran.

This guide provides a comprehensive overview of these topics, ensuring veterans have the information to make informed decisions about their home purchase and financing options.

Table of Contents

- What is a Gift Fund?

- Eligibility of Gift Donors for VA Loans

- Acceptable Gift Sources and Uses for VA Loans

- Guidelines for Personal Gift Funds

- Documentation for Personal Gift Funds

- What is A Gift of Equity, and How Can They Help Veterans?

- Frequently Asked Questions About Gift Funds for VA Loans

- Bottom Line

What is a Gift Fund?

A gift fund is a monetary gift provided by family members, friends, or other benefactors to assist with the purchase of a home.

These funds are particularly valuable in VA loans since they can be used for closing costs, down payments, or other mortgage-related expenses without the expectation of repayment.

By reducing the burden on veteran homebuyers, homeownership becomes more affordable and accessible.

The gift fund differs from a loan because it does not require repayment; the giver does not expect any return or compensation for the gift.

The approval and terms of VA loans depend on ensuring that gift funds are actually gifts. To utilize these funds effectively, veterans must adhere to VA guidelines and maintain proper documentation.

Eligibility of Gift Donors for VA Loans

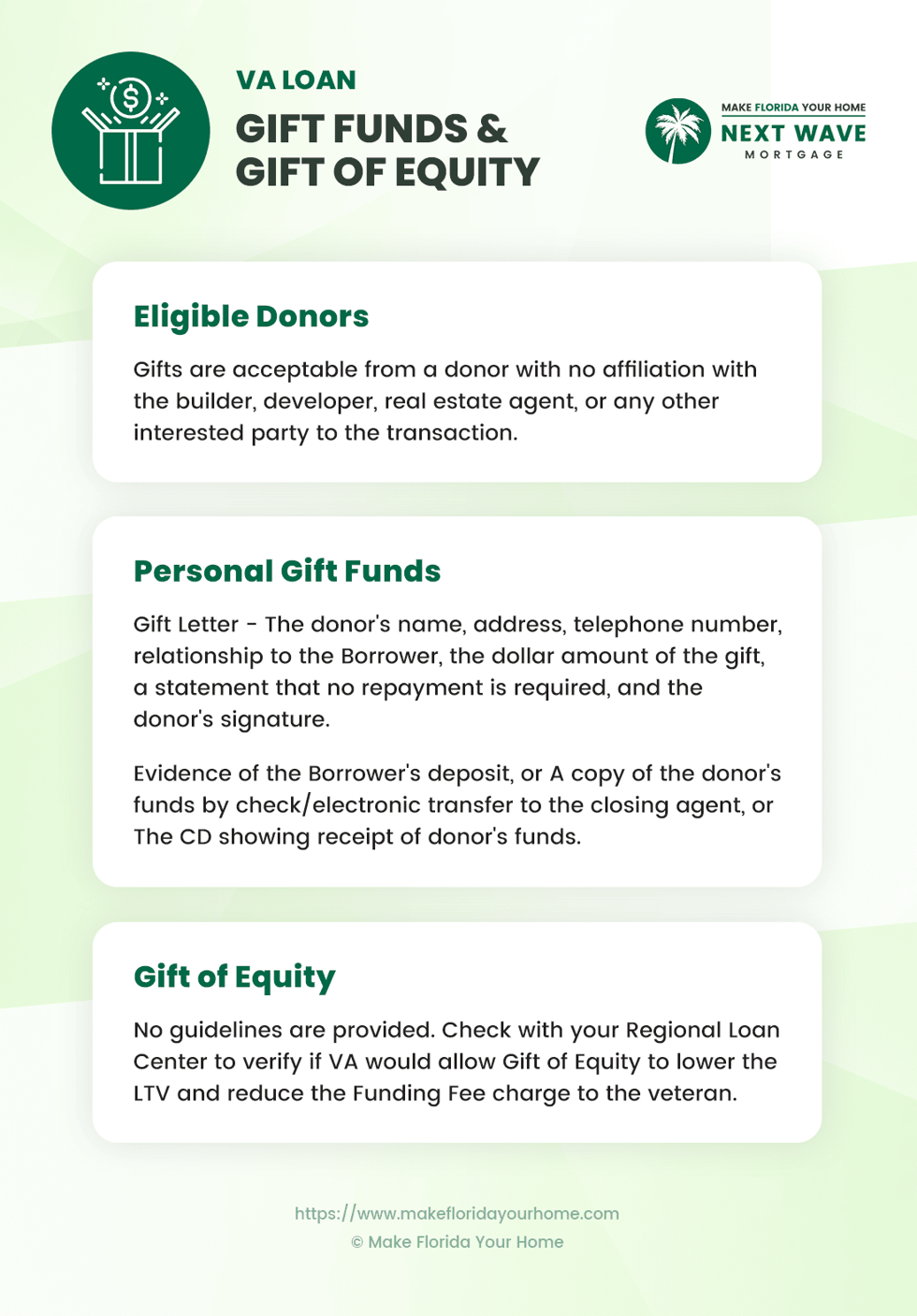

According to the VA Lenders Handbook, Chapter 4, 4-d, an eligible gift donor is defined as any individual who does not have an affiliation with the builder, developer, real estate agent, or any other interested party to the transaction.

As a result of this definition, family members, friends, and other generous contributors will be able to contribute to the veteran's home purchase without having any involvement in the sale.

By requiring a genuine gesture, the VA ensures that the gift is not being used to influence the transaction or to demand repayment.

"Gifts are acceptable from a donor with no affiliation with the builder, developer, real estate agent, or any other interested party to the transaction," as outlined in the Handbook.

This rule is designed to maintain the VA loan program's integrity and protect the veteran homebuyer's interests.

To prevent potential conflicts of interest or unethical arrangements which could disadvantage veterans, the VA requires that donors have no direct financial or personal interest in the sale.

Thus, the gift is focused solely on assisting the veteran in becoming a homeowner, reinforcing the commitment of the VA loan program to serve returning veterans.

Acceptable Gift Sources and Uses for VA Loans

Acceptable gift sources for VA loans are not explicitly limited by the U.S. Department of Veterans Affairs as long as the donor does not have an affiliation with the builder, developer, real estate agent, or any other interested party in the transaction.

However, common sources of gift funds that are generally accepted include:

-

Family Members: Parents, siblings, grandparents, children, aunts, and uncles can provide gift funds. Extended family members may also be considered acceptable donors.

-

Fiancés or Domestic Partners: Individuals with a longstanding relationship with the borrower that can be easily documented.

-

Close Friends: Friends who have a clearly defined and documented relationship with the borrower, indicating a significant personal connection that could logically support the gift.

-

Employers or Labor Unions: Organizations or entities the borrower is associated with, such as their place of employment or a labor union member.

-

Charitable Organizations: Non-profit organizations or community groups that assist veterans or homebuyers.

- Government Agencies or Public Entities: Programs offer veterans or first-time homebuyers homeownership assistance.

Under VA loan guidelines, an acceptable gift is a voluntary transfer of funds from the donor to the veteran borrower, with no expectation of repayment.

These gifts serve as a vital resource for veterans, aiding them in covering the financial requirements of purchasing a home.

The VA's approach to gift funds is designed to ensure these contributions are genuine gifts, thus supporting veterans in their path to homeownership.

Gifts under VA loan guidelines can be used for various purposes, making them a versatile tool for veterans' home-buying process.

Specifically, acceptable gifts include:

-

Down Payment Assistance: Gifts can be used to make the down payment on a home, making it easier for veterans to secure financing without needing personal savings.

-

Closing Costs: Gifts can cover closing costs, which are various fees for finalizing the mortgage. This can include appraisal fees, title insurance, and more.

-

Paying Off Debts: In some cases, gifts can be used to pay off debts to improve the veteran's debt-to-income ratio, a key factor in loan qualification.

- Prepaids: These are upfront costs paid at closing, including homeowner's insurance, property taxes, and initial escrow deposits.

The flexibility of using gifts for these expenses allows veterans to leverage the generosity of their network, thereby reducing the financial burden of purchasing a home.

This adaptability highlights the VA loan program's commitment to providing veterans with accessible pathways to homeownership, emphasizing the program's goal to honor those who have served by making the dream of owning a home more attainable.

Guidelines for Personal Gift Funds

The VA Lenders Handbook provides a foundational overview of gift funding acceptance within the VA loan process.

Still, it does not delve into extensive additional guidance regarding personal gift funds. Personal gifts should adhere to a few simple but crucial requirements due to the absence of detailed directives.

All parties involved are protected by these conditions to ensure that gift funds are indeed genuine gifts and are not expected to be repaid, maintaining the integrity of the loan process.

-

Donor Eligibility: Gifts must be from individuals without affiliation to the transaction, including builders, developers, real estate agents, or any other interested parties.

-

Gift Letter: A letter from the donor is required, including their name, address, telephone number, relationship to the borrower, the gift amount, a statement that no repayment is expected, and the donor's signature.

-

Evidence of Transfer: Documentation showing funds transfer from the donor to the borrower or closing agent, such as a bank statement or transaction receipt, is necessary.

- No Repayment: It must be clear that the gift is not a loan and that no repayment is expected or required.

The basic requirements for personal gifts are important for donors and recipients to understand. The VA emphasizes that gift funds must be sourced from individuals without affiliation to the real estate transaction, excluding builders, developers, real estate agents, or any related parties.

This guideline is designed to prevent conflicts of interest and ensure the gift's authenticity, supporting the veteran borrower's financial needs without compromising the transaction's impartiality.

Documentation for Personal Gift Funds

Specific documentation is required to accept and utilize personal gift funds within the VA loan process. This documentation verifies the gift's legitimacy and the donor's intentions, aligning with VA guidelines.

The necessary documents include:

Gift Letter Requirements

A comprehensive gift letter must accompany any personal gift funds. This letter needs to contain several key pieces of information to meet VA standards:

-

Donor's Name, Address, and Telephone Number: These details help identify the donor and provide contact information for verification purposes.

-

Relationship to the Borrower: Clarifying the relationship ensures that the donor has no prohibited interest in the real estate transaction.

-

Dollar Amount of the Gift: Specifies the amount given to the borrower.

-

Statement of No Repayment Required: This declaration is crucial, as it confirms the gift does not need to be repaid, distinguishing it from a loan.

- Donor's Signature: The signature verifies the donor's acknowledgment and agreement to the terms outlined in the gift letter.

Evidence of the Borrower's Deposit

In addition to the gift letter, evidence of the gift's transfer and receipt is required:

-

Copy of the Donor's Check/Electronic Transfer: This document provides proof of the gift's movement from the donor to the borrower or closing agent.

- Closing Disclosure (CD) Showing Receipt of Donor's Funds: The CD should reflect the receipt of the gift funds, further validating the transaction.

This documentation is necessary for properly handling personal gift funds within the VA loan framework. It ensures transparency, compliance, and the smooth progression of the loan application process, ultimately aiding veterans in securing financing for their home purchases.

What is A Gift of Equity, and How Can They Help Veterans?

A gift of equity involves the sale of a property below its market value, where the difference between the sale price and the market value is considered a gift of equity from the seller to the buyer. This concept is particularly relevant in VA loans when a family member sells the property to a veteran.

The equity, or the property's value not covered by the loan, effectively contributes to the veteran's home equity. This can significantly reduce the Loan-to-Value (LTV) ratio, which is the comparison between the amount of the loan and the value of the home.

A lower LTV ratio can benefit the borrower by potentially reducing the VA funding fee, a one-time fee paid to the Department of Veterans Affairs to help support the loan program.

Despite the potential benefits of a gift of equity, such as reducing the amount of cash a buyer needs at closing and possibly lowering the funding fee, the VA Lenders Handbook does not provide specific guidelines on gifts of equity.

The absence of detailed instructions means that accepting and using a gift of equity can depend on various factors, including lender policies and the interpretation of VA loan requirements.

Given this lack of guidance from the VA, it's important for veterans interested in using a gift of equity to consult with MakeFloridaYourHome or another trusted lender.

We can offer personalized advice and clarify whether a gift of equity is allowable in your situation. We can also provide information on required documentation and any additional steps to include a gift of equity as part of a VA loan transaction.

In summary, while a gift of equity can offer substantial financial benefits to veterans purchasing a home from a family member, navigating the process requires a careful approach.

By reaching out to MakeFloridaYourHome, veterans can ensure they meet all requirements and maximize the advantages available through the VA loan program.

Frequently Asked Questions About Gift Funds for VA Loans

Who can provide gift funds according to VA loan guidelines?

Gifts for VA loans can be provided by anyone who does not have an affiliation with the builder, developer, real estate agent, or any other interested party in the transaction. This ensures the integrity of the gift, confirming the sale of the property does not influence it.

What can gift funds be used for in a VA loan?

A VA loan can use gift funds for down payment, closing costs, or other loan-related expenses. This flexibility helps veterans and military personnel manage purchasing a home's finances.

Is there a limit to the amount of gift funds one can receive?

The VA does not limit the gift funds a borrower can receive. However, lenders may have their own guidelines, so it's essential to consult with your lender.

Do gift funds need to be repaid?

No, gift funds do not need to be repaid. The donor must provide a gift letter stating that the funds are a gift and no repayment is expected.

What documentation is required for gift funds in a VA loan?

For gift funds, the borrower must provide a gift letter from the donor that includes the donor's name, address, telephone number, relationship to the borrower, the amount of the gift, a statement that no repayment is required, and the donor's signature.

Can gift funds be used for the entire down payment on a VA loan?

Yes, gift funds can cover the entire down payment, provided the funds meet VA and lender guidelines and are properly documented.

What happens if the donor of the gift funds is affiliated with the real estate transaction?

Gifts from donors affiliated with the real estate transaction (e.g., builder, developer, real estate agent) are unacceptable under VA guidelines to prevent conflicts of interest.

How do gift funds affect the loan-to-value (LTV) ratio?

Gift funds used towards the down payment can lower the loan-to-value ratio, potentially improving loan terms and reducing the funding fee.

Can a family member provide gift funds?

Yes, family members can provide gift funds for a VA loan as long as they do not have any affiliation with the real estate transaction.

Are there any specific guidelines for gifts of equity in VA loans?

The VA Lenders Handbook does not provide specific guidelines for gifts of equity. Borrowers are advised to check with their Regional Loan Center for eligibility and documentation requirements regarding gifts of equity.

Bottom Line

Utilizing gift funds within the VA loan process offers veterans and active military personnel a significant advantage in achieving homeownership.

These funds, which can cover down payments, closing costs, and other loan-related expenses, provide financial flexibility and support. The key is ensuring that gift funds come from eligible donors and are properly documented according to VA guidelines.

By leveraging gift funds wisely, veterans can navigate the home-buying process more effectively, making the dream of owning a home more accessible and affordable.

With over 50 years of mortgage industry experience, we are here to help you achieve the American dream of owning a home. We strive to provide the best education before, during, and after you buy a home. Our advice is based on experience with Phil Ganz and Team closing over One billion dollars and helping countless families.

About Author - Phil Ganz

Phil Ganz has over 20+ years of experience in the residential financing space. With over a billion dollars of funded loans, Phil helps homebuyers configure the perfect mortgage plan. Whether it's your first home, a complex multiple-property purchase, or anything in between, Phil has the experience to help you achieve your goals.

About Editor - Ryan Skerritt

Ryan Skerritt has over 10+ years of experience in the residential financing space. With over two hundred and fifty million of funded loan volume, Ryan has the skill set to help any homebuyer configure the perfect mortgage plan.