By Phil Ganz

By Phil Ganz

Edited by Ryan Skerritt

Edited by Ryan Skerritt

In this guide, we'll explore co-borrowers' role in the FHA loan process, focusing on the benefits, limitations, and key considerations to remember as you embark on your home-buying adventure.

Table of Contents

- Challenges with Non-Occupant Co-Borrowers in FHA Loans

- Eligibility Criteria for Co-Borrowers

- Impact of a Co-Borrower on Loan Terms

- Risks and Responsibilities of Co-Borrowing

- Preparing for the Application Process

- Co-Signers vs. Co-Borrowers in FHA Loans: What's Different?

- Frequently Asked Questions (FAQ)

- The Bottom Line

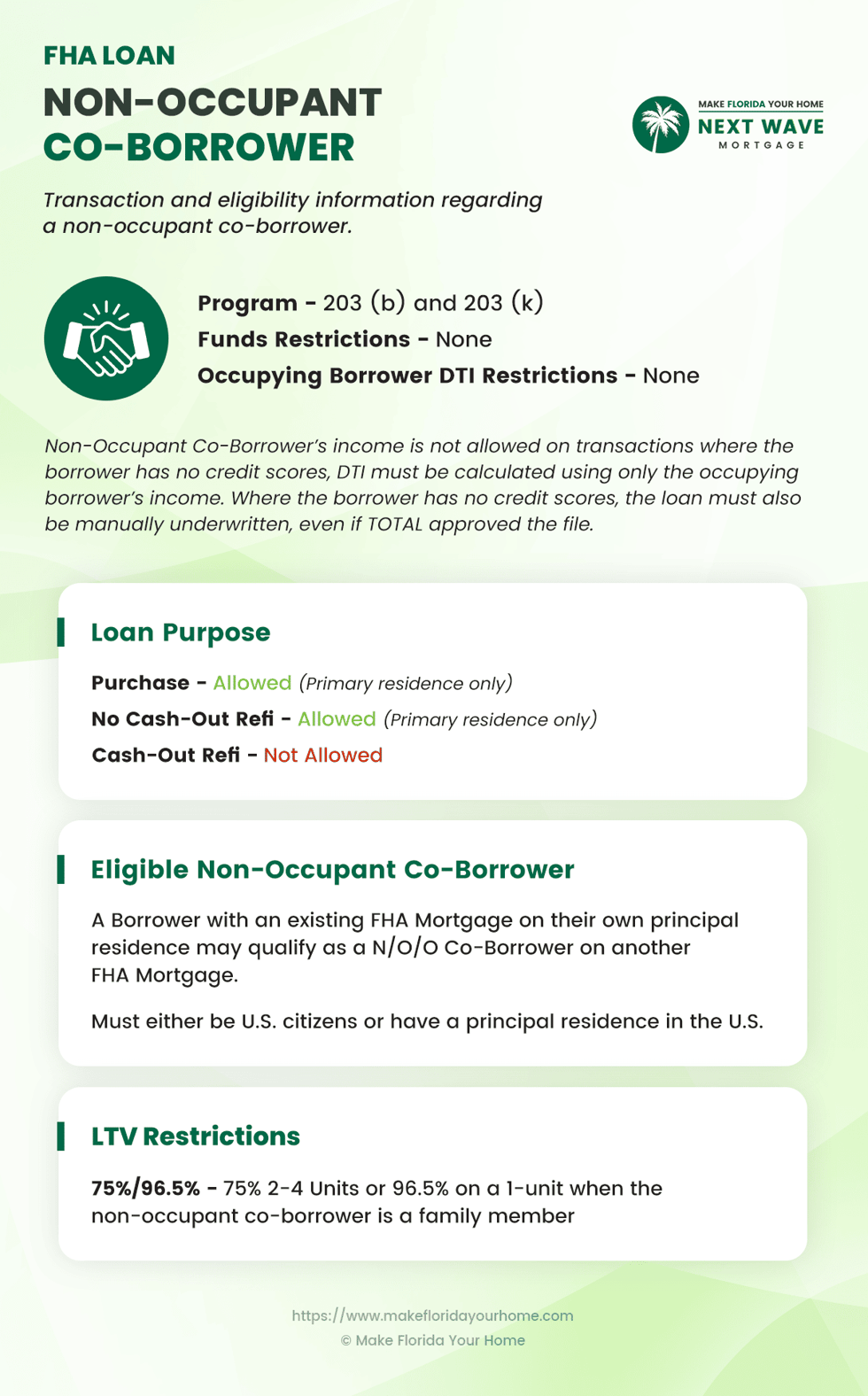

Challenges with Non-Occupant Co-Borrowers in FHA Loans

One significant challenge in the FHA loan process arises when the primary borrower lacks a credit score. In such scenarios, the FHA imposes specific restrictions on using the income of a non-occupant co-borrower.

This rule can be a major obstacle for those with a willing co-borrower ready to assist despite having insufficient credit history or income.

Typically, a co-borrower's financial strength, including income and credit history, is crucial in enhancing the loan application. However, without a credit score for the primary borrower, the FHA loan system limits the potential benefits a co-borrower can bring.

This can result in a challenging situation for aspiring homeowners who might be financially responsible yet lack the traditional credit background that lenders usually seek.

Eligibility Criteria for Co-Borrowers

When adding a co-borrower to an FHA loan, it's essential to ensure they meet specific eligibility criteria. Here's a checklist to guide you:

-

Family Relationship: Confirm that the co-borrower is a close family member (spouse, parent, sibling, or child).

-

Primary Residence Requirement: Ensure the co-borrower will occupy the property as their main home.

-

Stable Income: Verify that the co-borrower has a reliable and steady income source.

-

Credit Score Assessment: Check that the co-borrower has an adequate credit score.

- Debt-to-Income Ratio: The co-borrower should have a low debt-to-income ratio to demonstrate financial stability.

The FHA recognizes various familial relationships when considering co-borrowers for FHA loans. These relationships include immediate family members like spouses, children (including adopted and foster children), and parents (including step-parents and foster parents).

It also extends to siblings (including step-siblings), grandparents (including step and foster grandparents), aunts, uncles, in-laws (such as son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, and sister-in-law), and domestic partners.

Financially, they need a stable income, a suitable credit score, and a low debt-to-income ratio. These financial requirements help ensure that the co-borrower can reliably contribute to loan repayment.

Impact of a Co-Borrower on Loan Terms

Adding a co-borrower to an FHA loan can significantly influence the loan's terms. A co-borrower with a strong financial background can improve the overall creditworthiness of the application. This can lead to more favorable interest rates, reflecting the lower risk the lender perceives.

Additionally, with the combined income of the primary borrower and co-borrower, you might qualify for a higher loan limit, allowing you to purchase a more expensive property.

However, it's important to note that the co-borrower's credit history and financial situation will be thoroughly examined, as their financial liabilities will also impact the loan's terms.

The presence of a co-borrower can make a substantial difference in the affordability and reach of your home purchase.

Risks and Responsibilities of Co-Borrowing

Co-borrowing on an FHA loan involves significant legal and financial responsibilities. Both the primary borrower and the co-borrower are equally liable for the loan.

This means that in the event of a default, both parties' credit scores could be adversely affected. Furthermore, the co-borrower's debt-to-income ratio will be impacted as the loan obligation is reflected on their credit report.

This could influence their ability to obtain future loans. It's crucial for potential co-borrowers to understand these risks and to communicate openly about their financial situations and commitment to repaying the loan.

Preparing for the Application Process

Preparation is key when applying for an FHA loan with a co-borrower. Both parties should start by checking their credit scores and reports to understand their financial standing. It's important to correct any inaccuracies in these reports.

Gathering necessary financial documents is another critical step. This includes tax returns, pay stubs, bank statements, and other relevant financial information.

Both borrowers should also reduce their debt-to-income ratios, a crucial factor in loan approval. Thorough preparation can streamline the application process and improve the chances of approval.

To prepare for an FHA loan application with a co-borrower, consider the following checklist:

-

Credit Report Review: Both parties should obtain and review their credit reports, addressing any inaccuracies.

-

Financial Documentation: Gather key financial documents, including tax returns, pay stubs, and bank statements.

-

Debt-to-Income Ratio: Work on minimizing existing debts to improve this crucial metric for loan approval.

-

Budget Assessment: Evaluate your combined financial capabilities to determine a realistic budget for your home purchase.

- Open Communication: Discuss financial responsibilities and expectations openly to ensure a mutual understanding of the commitment.

Co-Signers vs. Co-Borrowers in FHA Loans: What's Different?

When navigating FHA loans, distinguishing between a co-signer and a non-occupant co-borrower is crucial for homebuyers.

A cosigner's role is primarily financial; they are obligated to the mortgage but don't hold any ownership interest in the property. This means they're responsible for loan payments if the primary borrower defaults but has no legal claim to the property.

In contrast, a non-occupant co-borrower has a more significant role. Not only are they similarly obligated on the mortgage note, but they also share ownership of the property.

At the closing, a co-borrower is required to sign all the security instruments, effectively listing the property in their liabilities. This shared ownership and financial responsibility make the co-borrower's role more extensive.

While a co-signer might be more readily found due to their limited involvement, a co-borrowers deeper financial and legal involvement in the property requires greater commitment and trust.

Frequently Asked Questions (FAQ)

You might have several questions when considering an FHA loan with a co-borrower.

Here are some of the most common inquiries we receive and concise answers to help you navigate this process.

Can a friend be a co-borrower on an FHA loan?

Friends generally do not qualify as co-borrowers for FHA loans, as co-borrowers are typically required to be family members.

Do both borrowers need to have the same employment history length?

No, the FHA does not require co-borrowers to have identical employment histories. Each borrower's employment history is assessed individually.

How does bankruptcy or foreclosure affect co-borrower eligibility?

A past bankruptcy or foreclosure can impact eligibility, typically requiring a waiting period before applying for an FHA loan.

Can a co-borrower be removed from an FHA loan in the future?

Yes, co-borrowers can be removed, which usually requires refinancing the loan.

Are non-U.S. citizens eligible as co-borrowers?

Non-U.S. citizens can be co-borrowers if they meet specific residency and documentation requirements.

Does a co-borrower's age impact FHA loan eligibility?

Co-borrowers have no age restrictions as long as they can legally enter into a mortgage contract.

Can a co-borrower contribute to the down payment?

Yes, co-borrowers can contribute to the down payment, which can help meet FHA loan requirements.

Are there any tax implications for a co-borrower on an FHA loan?

Co-borrowers may face tax implications, especially if they contribute to mortgage payments. It's advisable to consult a tax professional.

Can a co-borrower live in a different state?

A co-borrower can live in a different state, but they must still intend to occupy the property as their primary residence.

Does adding a co-borrower guarantee loan approval?

While it can improve chances, adding a co-borrower does not automatically guarantee FHA loan approval.

The Bottom Line

Adding a co-borrower to an FHA loan can be a strategic move to enhance loan eligibility and potentially secure more favorable terms. However, it's crucial to understand the responsibilities, risks, and eligibility criteria involved.

Both primary borrowers and co-borrowers should carefully consider their financial standing and the impact of such a decision on their future credit and homeownership journey.

Ultimately, the right preparation and knowledge can make co-borrowing a beneficial step toward achieving your home-buying goals.

With over 50 years of mortgage industry experience, we are here to help you achieve the American dream of owning a home. We strive to provide the best education before, during, and after you buy a home. Our advice is based on experience with Phil Ganz and Team closing over One billion dollars and helping countless families.

About Author - Phil Ganz

Phil Ganz has over 20+ years of experience in the residential financing space. With over a billion dollars of funded loans, Phil helps homebuyers configure the perfect mortgage plan. Whether it's your first home, a complex multiple-property purchase, or anything in between, Phil has the experience to help you achieve your goals.

About Editor - Ryan Skerritt

Ryan Skerritt has over 10+ years of experience in the residential financing space. With over two hundred and fifty million of funded loan volume, Ryan has the skill set to help any homebuyer configure the perfect mortgage plan.