By Phil Ganz

By Phil Ganz

Edited by Ryan Skerritt

Edited by Ryan Skerritt

Understanding these common obstacles is the first step to overcoming them. This guide aims to shed light on these challenges and offer actionable solutions to help you successfully qualify for an FHA loan in Florida.

Income Requirements

Understanding the Income Requirement Pitfalls in FHA loans can be intimidating. Our comprehensive approach explains them thoroughly, simplifying your journey to home ownership.

By comprehending and proactively handling FHA loan income requirements, you can boost your approval odds and accelerate your path to home ownership.

Proactively addressing income-related challenges in the FHA loan approval process can maximize your chances of success, allowing you to secure your dream home.

Minimum Income Threshold

Meeting the minimum income threshold for an FHA loan can be a hurdle for some. It's the FHA's way of ensuring you can handle mortgage payments. If this complexity seems daunting, professional advice can help navigate these more challenging waters.

If you're earning less than the FHA loan limit, strategizing to boost your income enhances your loan eligibility. Consider increasing work hours, seeking a higher-paying job, or utilizing side gigs.

Remember, FHA loans don't enforce a minimum income requirement; instead, they focus on your ability to repay the loan. Thus, low income doesn't necessarily mean disqualification. An impressive credit score or low debt-to-income ratio can significantly increase your chances.

Above all, always keep updated financial records. Lenders verify these records to assess loan affordability. Your wage statements, tax returns, and bank records should be in good order.

Ensuring you understand the nuances of the FHA's rules on minimum income requirements is critical. Sometimes, the interpretation varies between different mortgage companies. Remember, knowledge is power when navigating the home-buying process.

Documentation of Income

Proper income documentation is pivotal in FHA loans as it establishes your capacity to afford a mortgage. Determining final loan percentages and interest rates is critical to your loan approval process.

A comprehensive paper trail substantiating your income is crucial among common hurdles like fluctuating income or self-employment. This may include W-2s, tax returns, or pay stubs.

FHA loans often confront challenges of inconsistent or unconventional income. Nevertheless, covering two years of income verification bridges this gap and strengthens your loan application.

A crucial solution lies in thoroughly documenting all your income sources. This includes income from part-time work, bonuses, or alimony, enhancing your debt-to-income ratio.

While the process might seem extensive, accurately depicting your income and financial stability expedites your FHA loan approval. Remember, transparency and consistency are treasured in FHA loan income documentation.

Credit Score

Establishing a healthy credit score becomes pivotal for FHA loan approval. The Federal Housing Administration emphasizes lenders checking your creditworthiness and repayment capacity.

Addressing FHA loan hurdles can be made simpler through credit score enhancement. Regular bill payments, minimizing credit card balances, and rectifying credit report errors can precipitate an improved credit standing.

Minimum Credit Score

Securing FHA loans necessitates a minimum credit score. It forms an FHA loan challenge, yet it can be surpassed by improving credit behavior, timely payment, and debt reduction.

Typically, a credit score of 580 is the entry barrier for an FHA loan, enabling potential homeowners to access a 3.5% down payment. Those with lower scores may still qualify, yet with more extensive down-payment requirements.

Understanding the credit score barrier is crucial in FHA loan acquisition. This barrier, often a challenge, minimizes risk for the lender while protecting the market's stability.

A lower score increases the perceived risk for lenders, resulting in a higher down payment requirement. This rule guarantees the applicant's commitment and ability to fulfill loan obligations.

Thus, to overcome the challenge of a minimum credit score, maintaining a healthy credit behavior, clearing your outstanding debts, and avoiding late payments can develop a good credit score, easing the FHA loan process.

Credit History

Mastering the crafting of a robust credit history for FHA loans is paramount. Your payment track record and responsible credit behavior are significant in securing the loan.

Dealing with credit history discrepancies is inevitable. Quickly identifying and rectifying errors on your credit report can increase your chances of FHA loan approval.

Debt-to-Income Ratio

Understanding the debt-to-income ratio is fundamental in the FHA Loan process. This metric, measuring your total monthly debts against your gross monthly income, can significantly influence your loan approval chances.

Boosting your financial profile for a favorable debt-to-income ratio involves a two-fold strategy - increasing income or reducing debt. This can alleviate some challenges linked to acquiring an FHA loan.

Calculating DTI

Determining your Debt-to-Income (DTI) ratio is crucial to securing FHA loans. It's calculated by dividing your total monthly debt by your gross monthly income. This numerical value expressed as a percentage helps lenders assess your ability to manage monthly payments.

Misconceptions about DTI calculations often lead to confusion and decreased chances of loan approval. DTI isn't just about credit card debts or mortgages; it also includes student or auto loans, alimony, and child support.

Aim for a DTI ratio lower than 43% to improve your FHA loan eligibility. Lower ratios indicate that you have an adequate income to manage existing debts and a potential mortgage, making you more appealing to lenders.

Beware of the myth that a high income negates a high DTI. Despite substantial earnings, a high DTI signifies potential difficulty handling additional loan repayments. Always strive for a balanced DTI for a smoother FHA loan approval process.

DTI Limits

The Debt-To-Income (DTI) ratio limit is a critical hurdle in FHA loans; it dictates the ratio of your total monthly debt to your gross monthly income. This metric is crucial in evaluating a borrower's ability to reimburse the mortgage.

Falling short of the DTI limit? Adopting an inventive solution like paying down small debts or adding a significant other's income to the application can simplify your compliance with the FHA's DTI guidelines.

Property Requirements

Property requirements in FHA loans follow strict guidelines established by the Federal Housing Administration. Your adherence to these requirements can skyrocket your chances of loan approval. Our comprehensive guide decodes these standards, paving your way to property ownership.

Sailing through FHA loan property requirements can be overwhelming, with its fair share of hurdles. We help you navigate these challenges, ensuring a smoother journey towards your dream real estate investment.

Appraisal Compliance

Unlocking the secrets of FHA loan appraisal compliance eases potential mortgage hurdles. Beyond money and credit scores, homes must fare well under rigorous FHA appraisal. Recognizing this, savvy borrowers ensure properties meet agency standards.

Appraisal compliance poses a common obstacle in FHA loan processes. However, surpassing this challenge requires an understanding of what valuers focus on. The appraiser's eye lies on your prospective property's safety, security, and structural soundness.

Appraisal compliance is an unexpected ace in the FHA loan maze. A compliant property assists not just in loan approval but in negotiating fair prices, too. Invest time in learning and navigating compliance; it's worth the renewed peace of mind and financial safety.

Inspection Requirements

The FHA loan inspection process ensures the property is habitable and safe. The inspector, a professional approved by the Department of Housing and Urban Development, reviews the property's exterior and interior for structural integrity.

Failing the inspection doesn't mean the game is over; it opens an opportunity to negotiate repairs with the seller. Remember, a well-negotiated repair can turn a downside into an upside.

Approaching the inspection confidently and being prepared to tackle necessary repairs can help conquer FHA loan obstacles. A property falling short only means devising a new strategy staying within the goal.

In mastering FHA loan challenges, foreseeing possible repair issues can be part of your warrior's arsenal. Nimbleness and readiness can skirt potential roadblocks, ensuring a smoother journey to homeownership.

Mortgage Insurance Premiums

Mortgage insurance premiums (MIP) are integral to FHA loans, providing a safety net to lenders in case of buyer default. Decoding MIP consists of an upfront premium at closing and an annual cost spread across monthly payments.

Strategies to mitigate MIP-related challenges include paying the upfront MIP out of pocket to avoid increased monthly payments or considering a conventional mortgage alternative if the MIP significantly impacts the affordability of the property.

Upfront MIP

Understand that upfront Mortgage Insurance Premium (MIP) is a hurdle commonly encountered during FHA loans. It's a one-time, upfront premium paid at closing or financed into the loan. This element helps protect lenders from default-related losses.

The initial hurdle lies in comprehending the upfront MIP. However, fret not. There are strategies to minimize the impact of this challenge, leading to a smoother FHA loan process.

Alleviating this hurdle is achievable through strategic financial planning. Although the FHA requires the Upfront MIP, it can be rolled into your loan, thus easing the upfront cost at the closing table.

To further manage this hurdle, consider securing a loan with a lower principal amount. This solution effectively minimizes the amount of the upfront MIP, paving the way for a successful home purchase with FHA loans.

Annual MIP

The Annual Mortgage Insurance Premium (MIP) can be daunting for FHA loan applicants. Its inescapability forces borrowers to strategize around this obstacle to secure the loan successfully. By understanding the ins and outs of Annual MIP, they can strategically arrange for this additional fee.

Consider factoring the Annual MIP into your long-term financial planning to navigate this challenge. Converting this annual cost into a monthly expense can assist in better financial management, making the MIP payments less overwhelming.

Reprioritizing spending and budgeting for this MIP can assist borrowers in meeting this requirement without straining their finances. It's realistic planning that acknowledges the actual cost of an FHA loan.

Leveraging these strategies can ensure that the Annual MIP becomes an achievable hurdle, rather than a roadblock, in securing an FHA loan. A savvy approach takes the pressure off, transforming challenges into surmountable tasks.

Down Payment

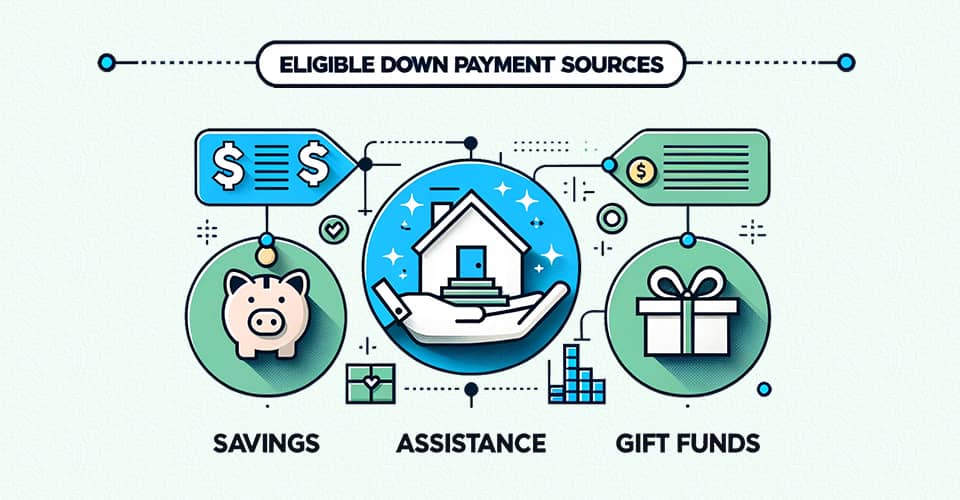

Addressing the down payment dilemma may seem daunting for prospective FHA loan applicants. However, sourcing funds from eligible down payment sources, such as savings or gift funds, can be a viable solution.

Crossing the down payment barrier for FHA loans requires effective strategies. For instance, supplementing personal savings with down payment assistance programs can help assignees reach the minimum needed more quickly.

Minimum Down Payment

Demystifying minimum down payments for FHA loans can alleviate buyers' anxiety. Based on the borrower's credit score, a purchase necessitates as little as 3.5% down. Consequently, home ownership becomes accessible, even for those with modest savings.

While traditional loans may mandate a higher percentage, FHA loans introduce flexibility. Borrowers can accumulate the necessary funds through various sources, including gifts from family or grants.

The puzzle of minimum down payments unravels with understanding. Familiarizing oneself with FHA loan requirements can turn the dream of homeownership into reality. Knowledge and preparation eliminate the barriers.

Alternative Down Payment Sources

There are a handful of alternative avenues to explore for prospective homebuyers encountering hurdles with the required down payment for an FHA loan.

Leveraging them can provide an effective workaround for this common obstacle, offering creative solutions to meet FHA loan requirements.

-

Gifts from family, friends, or employers that can contribute to the down payment.

-

Grants from not-for-profit organizations or local government agencies.

-

Loans from retirement or investment accounts.

-

Proceeds from selling an existing property, such as a car or home.

- Savings specifically from Individual Development Account (IDA) programs.

Loan Limits

When applying for FHA loans, navigating the landscape of loan limits can be a significant challenge. It's a major stumbling block that could deter potential homebuyers and real estate investors. This key aspect profoundly influences your borrowing capacity and, ultimately, your home-owning dream.

Understanding the intricate details of these loan limits in FHA loans can be instrumental in overcoming this hurdle. Therefore, learning about and fully grasping these nuances would provide a strategic solution to alleviate any possible concerns regarding loan limits.

-

Gaining knowledge on specific FHA loan limits based on counties and states.

-

Analyzing your financial situation to understand how much you can qualify for.

-

Revisiting your budgets to meet loan limit requisites.

-

Exploring the option of getting an FHA-approved appraiser to assess the property's value.

- Consider high-cost area loan limits if you plan to buy a home in expensive real estate markets.

With over 50 years of mortgage industry experience, we are here to help you achieve the American dream of owning a home. We strive to provide the best education before, during, and after you buy a home. Our advice is based on experience with Phil Ganz and Team closing over One billion dollars and helping countless families.

About Author - Phil Ganz

Phil Ganz has over 20+ years of experience in the residential financing space. With over a billion dollars of funded loans, Phil helps homebuyers configure the perfect mortgage plan. Whether it's your first home, a complex multiple-property purchase, or anything in between, Phil has the experience to help you achieve your goals.

About Editor - Ryan Skerritt

Ryan Skerritt has over 10+ years of experience in the residential financing space. With over two hundred and fifty million of funded loan volume, Ryan has the skill set to help any homebuyer configure the perfect mortgage plan.